Dubai: The difference between becoming debt-free and becoming a forever revolver is one thing: YOU.

You have to choose to tackle debt, not at the surface level but from its roots. How? DECIDE to be debt-free. Just decide.

Once you’ve made the decision that you’re no longer going to wander into debt, focus all your energy and money to paying off your debt — whatever it takes.

Shed that “victim mentality”, as US-based financial guru Dave Ramsey says and push on.

Once debt free, stay debt free.

Always remember that there are no easy or quick fixes. If you’re a revolver, it took time for your debt to balloon and accumulate.

Paying it off is the same.

There’s no magic formula; only your will power to get rid of it and live a debt-free life.

There are two ways to tackle multiple debts: snowball and avalanche. You may have already heard of both payment schemes but if you’re still into debt, maybe just hearing about it is not enough. Let’s break it down for you.

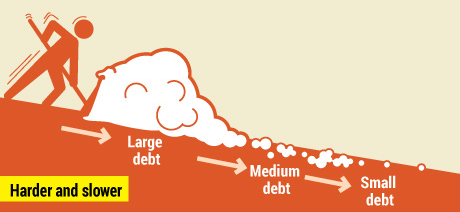

What is the debt snowball?

The debt snowball is similar to building a snowball in your backyard. You pick up some snow and form it into a ball and then roll it on the ground to pick up more snow until it becomes a huge one.

The debt snowball follows the same process. You list your all your debts — smallest to largest — and you attack the smallest by paying the maximum or paying it off. Pay the minimum for the rest. Take note that make the payments regardless of the interest rates.

For the next month, use the amount that you paid for the small debt to pay off the next debt on your list, paying minimum on the others, until you finish the whole thing off. Repeat until debt-free.

The method was popularised and advocated by Ramsey in his bestselling book ‘Total Money Makeover’. Ramsey says millions of Americans have become debt-free, paying off millions of dollars using this sure-fire method.

Does it work?

Yes. By paying off the smallest debt first, you create momentum and motivation to pay off the rest of your debt. The “small victories” create behavioural changes that keep you on fire to continue until you pay off everything and become debt-free, research shows.

How to succeed in debt snowball

- Starter emergency fund: Dave Ramsey only advises for you to start your debt snowball after setting aside $1,000 (Dh3,670) as a starter emergency fund. Adjust the amount to Dh1,000 or Dh3,000, whichever suits you. This way, you won’t go into debt in case of an emergency.

- Plastic surgery: If you’re financially bleeding, and profusely at that, the answer is not just blood transfusion. It’s to stop the bleeding. Cut up your credit cards by doing a “plasectomy”, as Ramsey puts it. This is when you DECIDE not to resort to debt anymore. Your mantra should be: “Never again.”

- Budget: Write your monthly budget before the month begins and include your debt repayment. Squeeze every dirham from your budget to go to debt repayment if they’re not for basic, again BASIC needs. Be radical. Ramsey calls it “scorched earth lifestyle” for a while. Close your eyes and imagine how life will be like with no payments.

- Be intense: Keep a reminder on your fridge or your wall or your diary of your debt repayment plan. There are a bunch of templates available online. Agree with your family that ALL of you have to commit to eliminating debt.

- Cash flow: Increase cash flow by getting a higher paying job and taking part-time jobs to add to your snowball. The UAE now allows this. Take advantage of it! A few hundred dirhams is a big help. Also, sell the “stuff” you’ve accumulated. Survive on a bare minimum and sell everything that’s not bolted down, as Ramsey puts it.

Will it save you a lot of money?

No, because you’re not tackling the debt with the biggest interest rate. But it will get you fired up. Again, this plan is not about Maths. It’s about changing behaviour.

Source: daveramsey.com

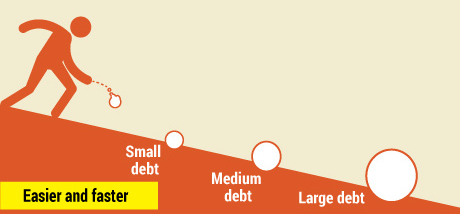

What is the debt avalanche?

As the name suggests, debt avalanche refers to debt repayment that prioritises the one with the highest interest rate and paying minimum for the rest. So list your debt with the highest interest rate first and with the lowest interest rate last.

Once you’re done paying off the highest interest debt, attack the next one. Repeat the process until you’re debt-free.

Does it work?

If we’re talking about Math, yes, it does. This method does not take into account the balances on your card, only the interest rates. So if you already have the discipline to pay off debt and have the cash for it, this will also work for you. For revolvers, we don’t recommend this approach as it’s mostly a person’s mind-set and spending habits that led him to being a revolver that needs to be dealt with.

Of the two, debt snowball is more effective according to research.

How to succeed in debt avalanche

- Apply the same principles listed in the debt snowball.

- The challenge with this method is keeping momentum. Paying off the highest interest rate debt might be daunting and you won’t have the small victories you’d have when you’re doing the snowball.

- So to keep you motivated, think of how much money you can save by ditching that high-interest debt. That’s your reward.

Will it save you a lot of money?

Yes. It’s the cheapest way to pay off debt as you will save on high interest that you would have otherwise accumulated while paying using the debt snowball.

• Interest: 18 APR (annual percentage rate)

• If your payment choice is: Minimum payment of $37 (Dh135.79) monthly

• Time it will take to repay the balance: 160 months (more than 13 years), assuming you don’t buy anything else with the card

• Total interest paid: $1,792.52 (roughly 20 per cent higher than the original owed at the start)

• If your payment choice is: If you add $10 a month to the minimum payment each month

• Time it will take to repay the balance: 44 months (less than four years)

12-18% is the percentage of how much you spend more when using credit cards versus cash