If investment is a journey, then asset allocation is its guiding star. Here are four steps towards building an investment portfolio that suits your needs.

Getting your investment portfolio right requires getting your asset allocation right. When it comes to returns, 80 per cent of the result can be attributed to asset allocation yet many investors don’t realise this. Whether you’ve recently inherited funds, turned a cash profit by downsizing or simply decided to start structuring your wealth, it pays to work through the four steps below.

Step one: Map-out your game plan

What would you like to achieve? And by when? No-one invests just for the sake of it – there’s always an expectation driving our investment behaviour. But we only know if our expectations are met when we truly understand them. This requires taking time to specify your needs in detail: What are the exact financial and wealth goals you wish to achieve? This can be more wide-ranging than we initially think, spreading past desired profit levels to include philanthropic or entrepreneurial goals, as well as the fulfillment of dreams such as home ownership, renovation or travel.

In determining your game plan, a lot will depend on your current life situation. Are you newly married and beginning a family? Have you recently inherited money or purchased real estate? Perhaps you’ve recently become single again or are thinking about remarriage? And then there are the important milestones of retirement and succession planning. It’s about finding the right balance between your current life and business situation, investment goals and financial aspirations. It’s important our investment portfolio suits both where we are today and where we hope to be in the future.

Step two: Pin down your investor profile

Once you’ve identified your goals in detail, it’s time to determine your investor profile. Begin by asking yourself “What’s my primary objective for the assets I own?” and see which investor profile suits you best:

Capital preservation: You want to preserve the level of capital you already have, while taking the least possible risk. If so, you’ll need to recognise and accept that the very limited growth and income potential of minimal-risk- and/or high-liquidity-instruments is balanced against their relative security.

Balanced risk: This involves investing in instruments of a minimal- to medium-risk type, recognising that there may be only limited growth potential. Such investors are looking for regular income from interest and dividend earnings, and are willing to absorb some risk of potential loss to capital.

Dynamic growth: Investors looking to grow the value of their investments and accumulate wealth over time through price appreciation. Instruments are of a higher risk type and therefore have greater potential to accumulate wealth. By accepting such risk, you trade short-term losses of a higher magnitude and greater year-on-year variance with above-average growth.

The two most important aspects you should consider in this regard are your risk tolerance and your financial knowledge and experience. The combination of your overall investment objective, risk tolerance and financial knowledge influences which investment strategy and asset allocation suits you best.

Step three: Picking the right strategy

The overall objective is to protect yourself against unnecessary losses and achieve long-term financial goals. Knowing your risk-tolerance and your risk-appetite is crucial to creating an investment plan you’ll have the nerves – and incentive – to stick with. A good check-in is to ask yourself two questions: “What financial risks can I bear?” and “What risks do I want to bear?”

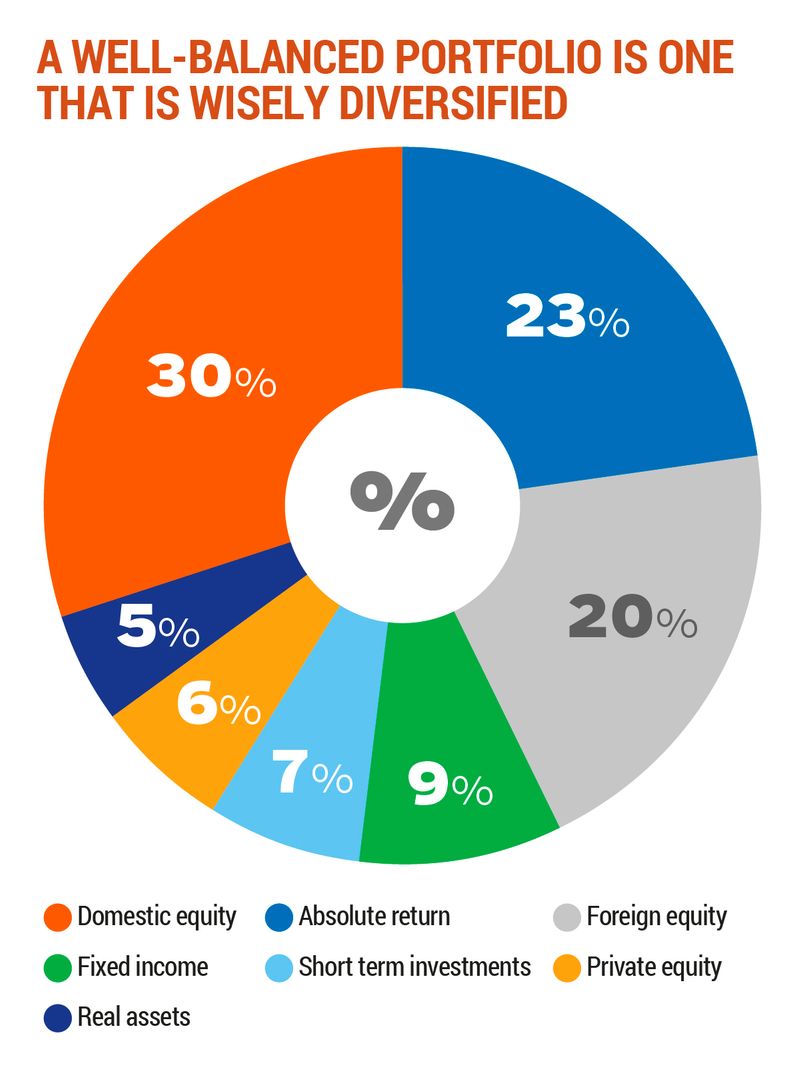

There are five key investment strategy types to consider: ‘Fixed income’, ‘Income’, ‘Balanced’, ‘Growth’ and ‘Yield’. Each strategy divides your investment portfolio among different asset categories, such as stocks, bonds and cash. The process of determining which mix of assets to hold in your portfolio is a very personal one and should reflect your current point in life, your investment timeline and your ability to tolerate risk.

It is essential to understand the basics of asset allocation, as it can influence up to 80 per cent of your average portfolio return. It’s also crucial to diversify across and within asset classes to lower the risk taken for the desired return. Gaining knowledge of and experience with different asset classes – money markets, bonds, commodities, shares and foreign exchange – puts you on the right path to selecting the ideal strategy and risk-return profile.

Step four: How will this work in reality?

By now it should be clear that asset allocation is the name of the game, with kick-off taking place long before you begin investing. Having worked out your goals, investor profile and suitable strategy, it’s time to put your assets to work. Here, there’s an analogy that rings particularly true: We’re often taught to take control of our lives, but when it comes to investing, once the groundwork is done, the best returns come from taking our hands off the wheel and practicing patience.

What does this mean in reality? The biggest risk to your investment return is your behaviour. Knowing your ideal investment strategy is not enough – it also needs to be deployed effectively. Picking the most appropriate investment strategy is a key risk-management step towards safeguarding your assets. This will be a personal decision for each investor, depending on factors such as their knowledge of asset classes and ability to remain professional as opposed to emotional about financial decisions.

This is where the decision between ‘discretionary’ versus ‘advisory’ comes in. Do you want to be in charge of managing your own assets, delegate the responsibility or opt for a combination of the two? The range of management option variations is endless but it ultimately needs to match your overall objective, risk tolerance and financial knowledge. And, in building an investment portfolio, the pay-off comes by sticking to your investment strategy. Keep this in mind when selecting your asset management approach and choose the style that will help you stay the course when things become unpredictable.

Diego Wuergler is the Head of Investment Advisory at Julius Baer